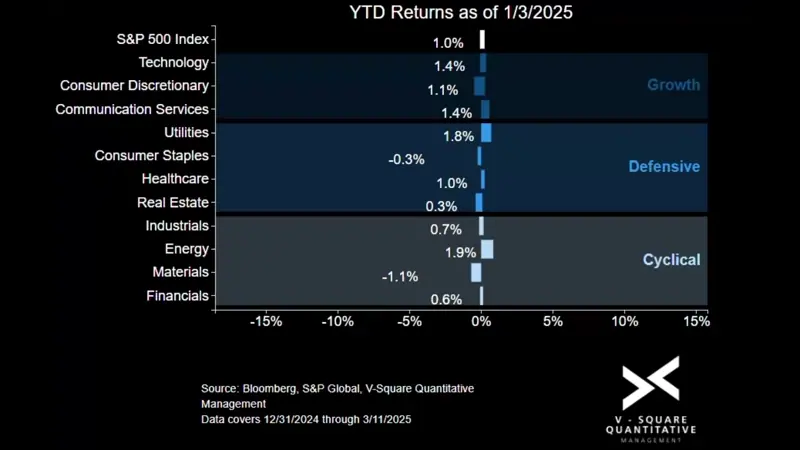

Over the past few weeks, the S&P 500 has declined steeply from its YTD high on February 19th, with concerns around tariffs, economic growth, and historically high valuations fueling volatility.

When considering the S&P 500 Index’s negative return YTD, we see significant dispersion across sectors. Growth-oriented sectors like Technology and Consumer Discretionary have borne the largest losses so far, reflecting a shift to risk-off positioning. Though we are still in Q1, the “Magnificent Seven” growth in 2025 is showing signs slowing.

By contrast, defensive sectors such as Healthcare and Consumer Staples have delivered positive YTD returns. Healthcare is showing a steady demand as the long-term tailwind of an aging population and reasonable valuations may be drawing investor interest after a few years of muted performance. Meanwhile, cyclical segments, such as Energy and Industrial, have remained relatively subdued YTD.

Are we in for a change in top-performing sectors or is this a short-term shift? Share your thoughts!

Source: Bloomberg, S&P Global, V-Square Quantitative Management. This chart illustrates the YTD Price Return from 12/31/2024 through 3/11/2025 for the S&P 500 Index and its underlying GICS Level 1 Sector Indexes. The “Magnificent Seven” stocks, a group of high-performing U.S. stocks in 2024, includes Tesla, Nvidia, Apple, Alphabet, Amazon, Microsoft, and Meta.

This chart is for illustrative purposes only. Other indexes are available. It is not possible to invest directly in an index. Index returns do not reflect any management fees, transaction costs or expenses. Past performance does not guarantee future performance. The information and opinions contained herein are for informational purposes only, do not purport to be full or complete, do not constitute investment advice and may not be relied on. For more information, please see vsqm.com/disclaimer.