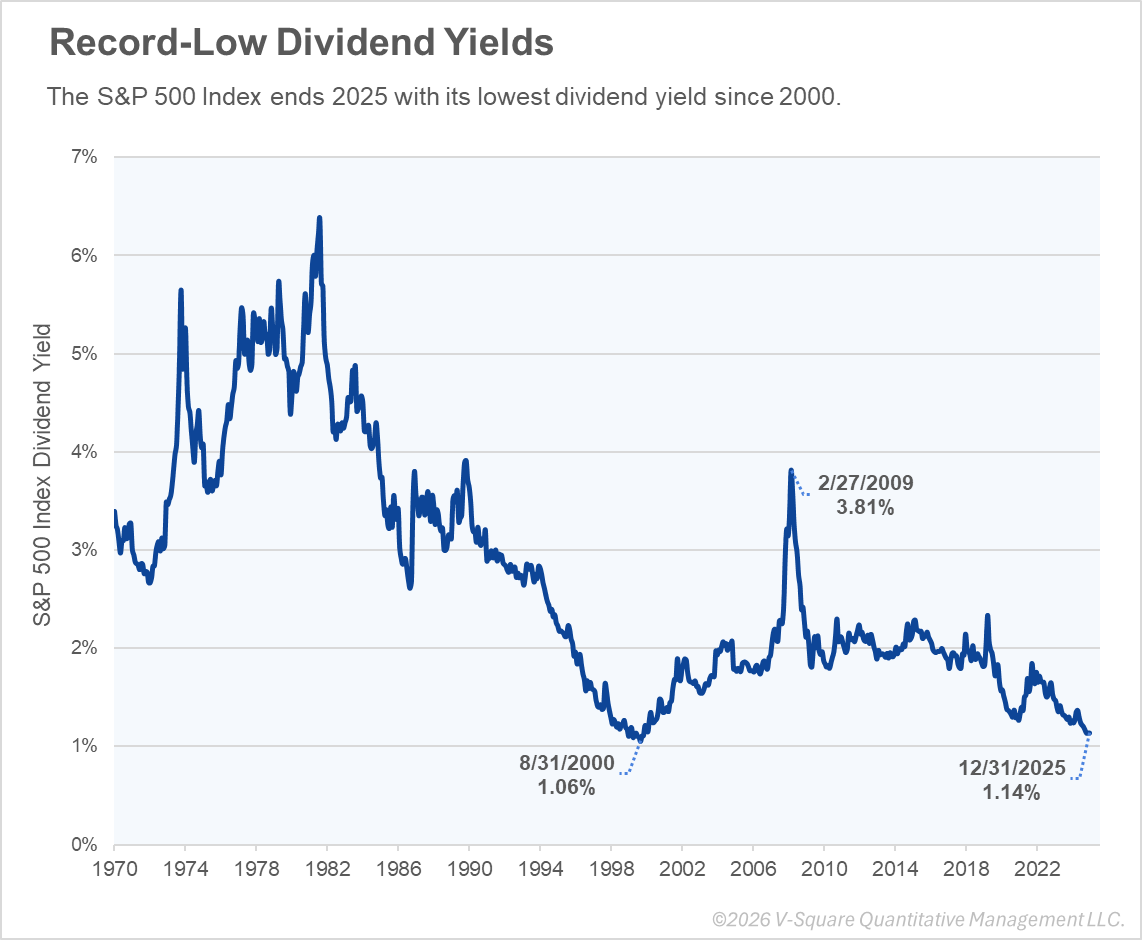

The S&P 500 Index closed out 2025 with a dividend yield of 1.14%, its lowest level since 2000 and far below its long‑term average of around 2.5-3%. In practical terms, investors today are earning a fraction of the income that large‑cap U.S. equities have historically provided.

While there are a number of factors contribuing to lower dividend yields today, for income focused investors, this difference can make a notable impact on portfolio-level yields. However, in our view, investors shouldn’t have to chose between equity upside potential and compelling levels of income.

By focusing on high dividend yielding companies with a quality component (e.g., strong balance sheets, durable free cash flow, etc.) we believe investors can increase the compounding benefits of dividends while still holding potential for long-term appreciation.

Focusing on this quality‑dividend segment can also help to potentially diversify portfolios that have become skewed toward a narrow group of mega‑cap growth names. In a market that is both top‑heavy and low‑yielding, investors being intentional about where their equity income comes from can help to reshape the risk and return drivers of the overall portfolio.

How do you think about dividend investing in your portfolio?

Source: Bloomberg, V-Square Quantitative Management LLC, S&P Global. Chart displays trailing 12-month dividend yield for the S&P 500 Index from December 31, 1970, to December 31, 2025.

This chart is for illustrative purposes only. Other indexes are available. It is not possible to invest directly in an index. Index returns do not reflect any management fees, transaction costs or expenses. Past performance does not guarantee future performance. The information and opinions contained herein are for informational purposes only, do not purport to be full or complete, do not constitute investment advice and may not be relied on. For more information, please see vsqm.com/disclaimer.